Don’t forget to account for the “accounting”

by Chris Biggs

When it comes to business transactions such as M&A, trade sales, equity or debt raises, dual track transactions or public listings, accounting workstreams are often considered secondary to the more exciting aspects of the deal.

However, neglecting accounting workstreams can lead to significant risks including:

- Failing to close the deal on time;

- Failing to obtain the required auditor or reporting accountant’s sign-off;

- Not producing the necessary information for the deal documentation; and

- Not fully understanding the deal’s accounting implications and complexities.

We have seen all these consequences occur when accounting workstreams are not considered until late in the process.

It is highly advisable and necessary to plan end-to-end for when the information generated by the accounting workstreams is required. The consequences of not doing this can be ‘deal fatal’ in many ways, including where regulatory signoffs and the age of financial information is strictly regulated. For example, in certain regulated deals, if financial information is too old (this could be as recently as 4 months post-period end), it is deemed stale, and more recent accounting periods are required to be produced and included. Such periods are often not yet available and may not have been so robustly produced with the transaction completion in mind.

To ensure a smooth transaction, it is crucial to incorporate key accounting workstreams in the overall project timeline from the very start – indeed some may be completed as part of getting ready for the deal process to commence.

It is often considered best practice to plan well ahead of other workstreams starting and we are often engaged by clients to start these accounting workstreams before a deal formally commences.

Accounting workstreams may include:

- Financial statements/ information;

- Working capital modelling; and

- Post-transaction governance environment.

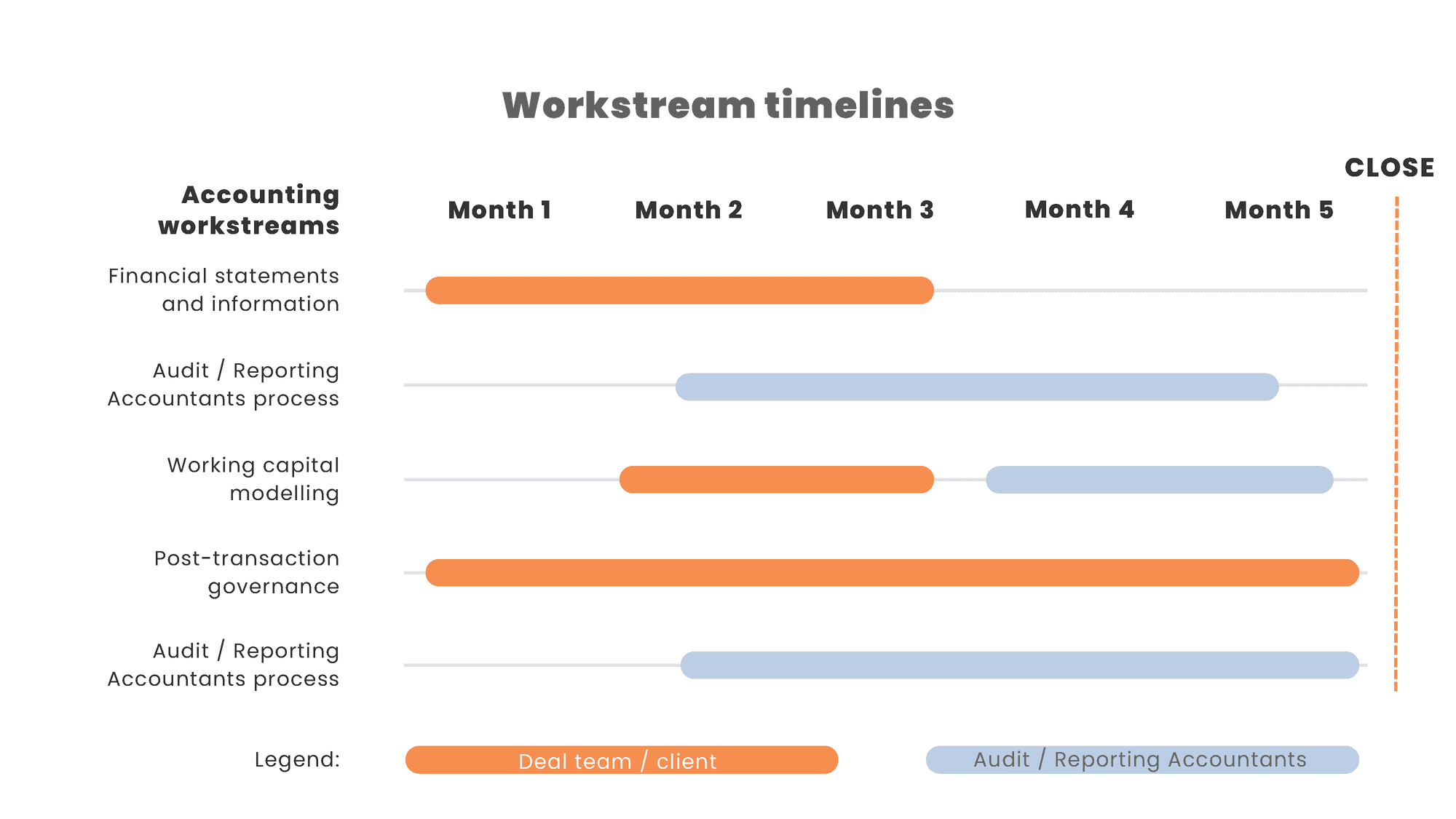

Below is a sample timeline for these workstreams (the indicative estimate will vary for each deal but this shows the significant time needed):

1. Financial statements/information (Estimated timeline: up to 3 months)

What is required:

The preparation of financial statements and financial information covering a certain historic period under fully compliant formal GAAP. This can include the conversion of financial information from the entity’s existing GAAP to new GAAP, or to the GAAP and policies of the acquiror. This can be required as part of the overall deal information package or for inclusion in the formal prospectus.

The process can involve:

- Detailed conversion of the target’s financial statements from their current GAAP to (for example) IFRS, US GAAP, or the soon-to-be parent’s GAAP;

- Complex calculation of GAAP conversion adjustments for all periods;

- Preparation of formal financial statements with footnotes for several years; and

- Auditing of the financial statements by an auditor or reporting accountant.

Key challenges include:

- Ensuring all required financial information is available for all required years;

- Tightly managing the auditor/ reporting accountant process; and

- Completing the complex calculations in areas such as financial instruments, lease accounting, credit-loss provisioning, and revenue recognition.

2. Working capital modelling (Estimated timeline: up to 2 months)

What is required:

Working capital modelling is a complex process. It necessitates constructing detailed monthly profit and loss, balance sheets, and cash flow forecasts often for at least 18 months into the future, all with a level of disaggregation of revenue and costs by business operation.

Reporting Accountants often ask for up to three years of historic data to be included in these models. Additionally, overlaying an analysis of cash headroom and including stress testing functionalities means this is a complex and lengthy process and can be very demanding on an already stretched finance team.

Early engagement with all parties involved in the process is essential, as is defining the required functionality to stress test the model and incorporating assumptions.

Key challenges include:

- The availability of all necessary information and forward-looking projections to create a comprehensive model of working capital under various scenarios;

- The sheer amount of work required to prepare a model capable of demonstrating multiple scenarios (e.g. a base case, a reasonable worst case, and other ‘stressed’ cases); and

- The need to reflect GAAP adjustments in the model if a GAAP conversion has occurred, meaning more GAAP conversion calculations for future periods.

3. Post-transaction governance (Estimated timeline: up to 5 months)

What is required:

In certain deals, especially those by listed or soon to-be-listed entities, the acquiror/ parent is required to demonstrate that they have established suitable governance procedures that allow directors to operate the ‘go-forward’ business in a suitable risk- managed manner.

Key challenges include:

- Directors will need to document that they formally accept responsibility for the requirements;

- The directors’ statement above must be based on auditable work they have completed; and

- Providing third party assurance over this directors’ statement, which requires the auditors/ reporting accountants to audit the control environment including new controls put in place to manage the new business.

We have seen real-life deal timelines derailed by this workstream alone, given the time needed for the company to assess and remediate control weaknesses, and often the considerable time the auditors/ reporting accountants need to complete their work and test the operation of certain controls for one or two cycles.

Closing thoughts

As you can clearly see, accounting workstreams are complex and time consuming and therefore must be incorporated from the outset of a deal being considered.

Proper planning, diligent execution of these workstreams, and experienced advisors can ensure a smooth transaction and avoid any derailment or unforeseen complications that could arise.

Photo: David - stock.adobe.com

/https://storage.googleapis.com/ggi-backend-prod/public/media/3192/office-a514885250.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/1936/imageiKobMB.png)

/https://storage.googleapis.com/ggi-backend-prod/public/media/451/imageKllmAI.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/5334/Handschlag---shutterstock_2021639264---square.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/4746/Swati-Rungta-impact-of-AI-on-accounting.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/4938/IMG_5896-square.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/3253/accountant-a587412905.jpg)